July 2021 Newsletter

Happy 4th of July! - Covenant Care

The 4th of July will be a day of food, fireworks and maybe a parade or concert. But it can also include prayer.

1. Give thanks for your freedom and favor.

2. Pray for those who protect our freedom.

3. Pray for our nation’s leaders.

4. Pray for the safety of those who gather to celebrate the holiday.

5. Remember those in oppressive or disadvantaged circumstances.

6. Find new freedom in forgiveness.

When We Get Too Weary (Galatians 6:9)

By Anne Peterson

And let us not grow weary of doing good, for in due season we will reap, if we do not give up. - Galatians 6:9

Let’s face it, we all get weary. Wiping the sleep out of our eyes, we know that we’re doing what we’re supposed to be doing. A pandemic was one of the worst things some of us have been through. It is scary to see the infection numbers and the rising count of those lost. Even though we know, at least here in America, that following the guidelines is helping. We are doing what is good. But even that can be taxing.

And sometimes, we look around and see others who are not following suit. And inside of us rises similar feelings like that of the prodigal son’s brother. Here he had been the obedient one and yet, when his prodigal brother returned, he saw his father run to him. Put a robe on his back and a ring on his finger (Luke 15: 11-32).

Sometimes it’s hard to do the right thing when everyone is not complying. And sometimes, like Peter who saw John coming and wondered what John’s position would be with Jesus (John 21:20-22). Instead of just doing what we know we should be doing, we start wondering about others.

What do we do when we get weary? When we think we can’t keep going? The answer is to go to the one who never tires or grows weary (Isaiah 40:28).

God tells us that he will strengthen us and help us (Isaiah 41:10).

He tells us when our strength starts waning, he will renew it and we will soar like eagles (Isaiah 40:31).

And when we think we can no longer do what is asked of us, like Paul we can recognize the source of our strength (Philippians 4:13).

We rise and go through the motions, often feeling helpless. But we must remember that God is sovereign. We are not in this alone. God has promised that he would never leave us nor forsake us (Hebrews 13:5-6). And God is not a man that he should lie (Numbers 23:19).

We are not alone. So do not grow weary in doing good.

With Me

I told the Lord, “This journey’s long,

He said, “I know the length.”

I told Him, “But I’m faint and weak.”

He said, “I’ll give you strength.”

No matter what my words—God heard;

He listened patiently.

But what has meant the most is this,

my Father walks with me.

-Anne Peterson

How Well Do You Understand Retirement Plan Rules?

Qualified retirement plans, such as IRAs and 401(k)s, have many rules, and some of them can be quite complicated. Take the following quiz to see how well you understand some of the finer points.

1. You can make an unlimited number of retirement plan rollovers per year.

A. True

B. False

C. It depends

2. If you roll money from a Roth 401(k) to a Roth IRA, you can take a tax-free distribution from the Roth IRA immediately as long as you have reached age 59½.

A. True

B. False

C. It depends

3. You can withdraw money penalty-free from both your 401(k) and IRA (Roth or traditional) to help pay for your children’s college tuition or to pay for health insurance in the event of a layoff.

A. True

B. False

C. It depends

4. If you retire or otherwise leave your employer after age 55, you can take penalty-free distributions from your 401(k) plan. You can’t do that if you roll 401(k) assets into an IRA.

A. True

B. False

C. It depends

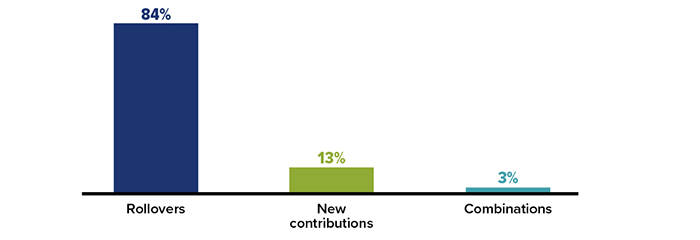

Shares of Traditional IRA Assets Opened with...

Shares of traditional IRA assets opened with rollovers=84%, new contributions=13%, and contributions=3%.

1. C. It depends. Rollovers can be made in two ways — through a direct rollover, also known as a trustee-to-trustee transfer, in which you authorize the funds to be transferred directly from one account or institution to another, or through an indirect rollover, in which you receive a check in your name (less a required tax withholding) and then reinvest the full amount (including the amount withheld) in a tax-deferred account within 60 days. If the full amount is not reinvested, the outstanding amounts will be considered a distribution and taxed accordingly, including any applicable penalty. Generally, individuals can make an unlimited number of rollovers in a 12-month period, either direct or indirect, involving employer-sponsored plans, as well as an unlimited number of direct rollovers between IRAs; however, only one indirect (60-day) rollover between two IRAs is permitted within a 12-month period.

2. C. It depends. Beware of the ?ve-year rule as it applies to Roth IRAs. If you establish your ?rst Roth IRA with your Roth 401(k) rollover dollars, you will have to wait ?ve years to make a quali?ed withdrawal from the Roth IRA, regardless of how long you've held the money in your Roth 401(k) account, even if you are over 59½. However, if you have already met the ?ve-year holding requirement with any Roth IRA, you may take a tax-free, quali?ed withdrawal.

3. B. False. You can take penalty-free withdrawals from an IRA, but not from a 401(k) plan, to pay for a child’s qualifying education expenses or to pay for health insurance premiums in the event of a job loss. Note that ordinary income taxes will still apply to the taxable portion of the distribution, unless it’s from a Roth account that is otherwise qualified for tax-free withdrawals.

4. A. True. If you leave your employer after you reach age 55, you may want to consider carefully whether to roll your money into an IRA. Although IRAs may offer some advantages over employer-sponsored plans — such as a potentially broader offering of investment vehicles — you generally cannot take penalty-free distributions from an IRA between age 55 and 59½ as you can from a 401(k) plan if you separate from service. If you might need to access funds before age 59½, you could leave at least some of your money in your employer plan, if allowed.

When leaving an employer, you generally have several options for your 401(k) plan dollars. In addition to rolling money into an IRA and leaving the money in your current plan (if the plan balance is more than $5,000), you may be able to roll the money into a new employer’s plan or take a cash distribution, which could result in a 10% tax penalty (in addition to ordinary income taxes) on the taxable portion, unless an exception applies.

Saving vs. investing explained

Saving is the act of putting away money for a future expense or need. When you choose to save money, you want to have the cash available relatively quickly, perhaps to use immediately. However, saving can be used for long-term goals as well, especially when you want to be sure you have the money at the right time in the future.

Savers typically deposit money in a low-risk bank account. Those looking to maximize their earnings should opt for the highest annual percentage yield (APY) savings account they can find (as long as they can meet the minimum balance requirements).

Investing is similar to saving in that you’re putting away money for the future, except you’re looking to achieve a higher return in exchange for taking on more risk. Typical investments include stocks, bonds, mutual funds and exchange-traded funds (ETFs). You’ll use an investment broker or brokerage account to buy and sell them.

If you’re looking to invest money, you should plan to keep your funds in the investment for at least five years. Investments can be very volatile over short periods of time, and you can lose money on them. So, it’s important that you only invest money that you won’t need immediately, especially within a year or two.

Short and Long Term Goals - MAX Credit Union

So which is better – saving or investing?

Neither saving or investing is better in all circumstances, and the right choice really depends on your current financial position.

Generally, though, you’ll want to follow these two rules of thumb:

If you need the money within a year or so or you want to use the funds as an emergency fund, a savings account or CD is your best bet.

If you don’t need the money for the next five years or more and can withstand some losses in capital, then you likely should invest the money.

Real-life examples are the best way to illustrate this, Keady says. For example, paying your child’s college tuition in a few months should be in savings — a savings account, money market account or a short-term CD (or a CD that’s about to mature when it’s needed).

“Otherwise people will think, ‘Well, you know, I have a year and I’m buying a house or something, maybe I should invest in the stock market,’” Keady says. “That’s really gambling at that point, as opposed to saving.”

And it’s the same for an emergency fund, which should never be invested but rather kept in savings.

“So if you have an illness, a job loss or whatever, you don’t have to resort back to debt,” Hogan says. “You’ve got money you’ve intentionally set aside to be a cushion between you and life.”

And when is investing better?

Investing is better for longer-term money — money you are trying to grow more aggressively. Depending on your level of risk tolerance, investing in the stock market, exchange-traded funds or mutual funds may be an option for someone looking to invest.

When you are able to keep your money in investments longer, you give yourself more time to ride out the inevitable ups and downs of the financial markets. So, investing is an excellent choice when you have a long time horizon (ideally many years) and won’t need to access the money anytime soon.

Reminder

If you would like to schedule some time with your advisor, please feel free to call (912)387-0111. We would love to get together with you!

Blessings!